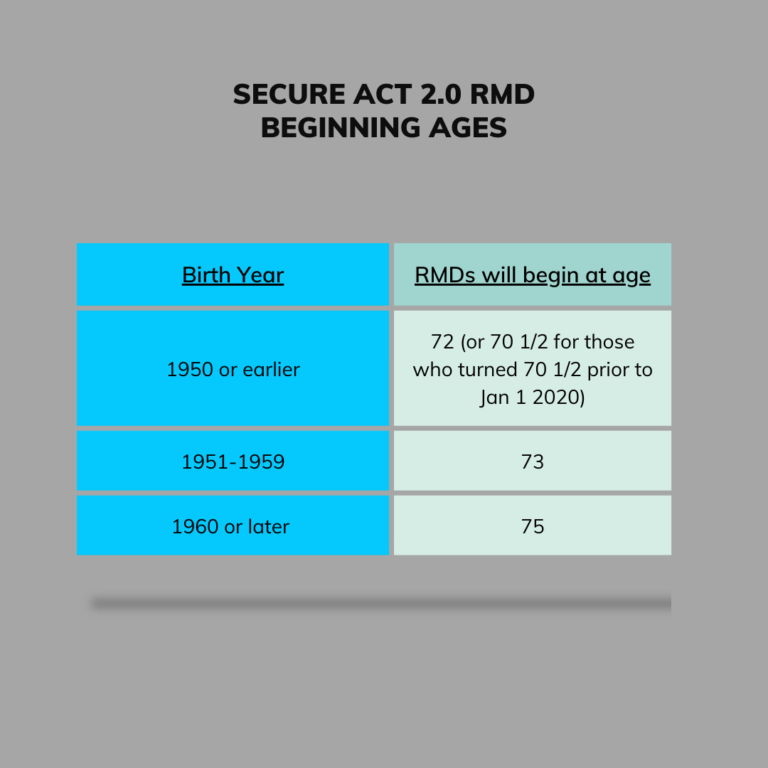

For those of you turning 72 in 2023, you were probably planning to have your beginning date start this year. However, this new legislation is in effect NOW, so your beginning date is 2024 when you turn 73! Happy Birthday to those born in 1951!

The next group of individuals born in 1960 or later will have a beginning date of the year they turn 75.

For the first RMD only, you can delay the distribution until April 1st of the following year.

For example, you turn 73 in 2024 (born in 1951). You can either take your first RMD in the calendar year of 2024 OR take that RMD by April 1st of 2025. Just remember, if you decide to delay until April 1st, you will have TWO RMD’s for 2025 (one for 2024, and one for 2025). However, this is helpful if your taxable income will drop substantially after your beginning date due to retirement or other reasons.

Planning opportunities for RMDs

First and foremost, SECURE Act 2.0 gives account owners more time until they are required to start taking RMDs. For many of you, you might be dreading RMDs as you might not NEED those distributions for income. Perhaps your Social Security, Pension, and other investment income is more than enough to live your lifestyle. Therefore, RMDs are more of a tax liability than anything else.

For some, considering a Roth conversion strategy could be advantageous.

Consider someone who is retiring at 62, and their earned income goes to 0. Perhaps they plan to live on their investment assets until reaching 70 (their Latest Retirement Age for maximum Social Security benefits). Assuming the beginning date is the year in which they turn 75, they have 13 years of potentially low income.

Therefore, instead of continuing to defer their retirement account balances until 75, one might consider converting portions of those existing tax-deferred account balances for the next 13 years. Yes, a Roth conversion would trigger taxes now based on the amount converted, but this also reduces the calculation for the RMD each year. Roth IRAs do not have RMDs, and distributions from Roth IRAs are tax-free (assuming they are qualified). Therefore, this could result in tax savings beginning at age 75, and could potentially last for 20+ years based on one’s life expectancy. I wrote an article on Roth conversions and if you should consider them that you can read here.

Another positive change is the elimination of the RMD from Roth 401ks and other Roth-qualified retirement plans. In the past, ONLY Roth IRAs were excluded from RMD calculations. Beginning in 2024, qualified plans with Roth balances will NOT be required to take an RMD.