6 Reasons to Take Advantage of a Roth Conversion

While I recently outlined reasons to steer clear of a Roth conversion, today I’m flipping the coin to explore when it can be a smart, strategic move for your financial future.

Why Consider a Roth Conversion During Market Downturns

A Roth conversion can be particularly beneficial during market downturns. When the market is down, you’re essentially exchanging a number of shares based on the dollar amount you want to convert from your tax-deferred account (whether it’s an IRA or a 401k) into a Roth.

You’ll have to pay taxes now in exchange for tax-free growth, which is the advantage Roth accounts offer. When markets are down, you can convert more shares with the same dollar amount.

For example, if you were looking to convert $50,000 worth of Vanguard’s Total Index (VTI) back in 2022 (the last bear market), you’d be able to convert an additional 25% worth of shares because the market was down roughly 25% that year. Just a thought, given we had some rough patches this April with the tariff concerns. We could continue to see more volatility in the months ahead.

While we can’t control market volatility, we can control smart tax planning. Let’s jump into the top six reasons you may consider a Roth Conversion in your financial planning strategy.

1. For Accumulators: Backdoor Roth IRA Strategy

The first reason is actually for people who are pre-retirement, or what I call “accumulators.” There are income thresholds for single and married filing jointly to directly contribute to a Roth IRA. If you fall into that category, the Roth conversion or backdoor Roth IRA strategy comes into play.

Essentially, you’ll make a non-deductible contribution into an IRA and then convert those assets into a Roth IRA. There are some tax traps you might fall into (the aggregation rule), so consult with your tax planner or financial planner before making this move. This strategy is available for IRAs, and sometimes, for 401ks as well. Contribution limits are much higher for 401ks than IRAs. If you have this option within a 401k, this could really boost your retirement savings.

2. Tax-Free Growth Long-Term

Reasons 2 through 6 are for individuals nearing retirement who have accumulated substantial savings in tax-deferred IRAs or 401ks.

The second reason is for long-term tax-free growth. If you believe tax rates probably aren’t going down and are more likely to go up or stay the same, then tax-free growth and compounding interest are much more powerful than tax-deferred growth. This could be for legislative reasons, or even simply projecting out your lifetime tax brackets. We know now that the One Big Beautiful Bill Act has made the current brackets permanent. Still, that doesn’t mean YOUR tax bracket might rise over time based on changes in your income or assets.

3. Eliminate or Reduce Required Minimum Distributions

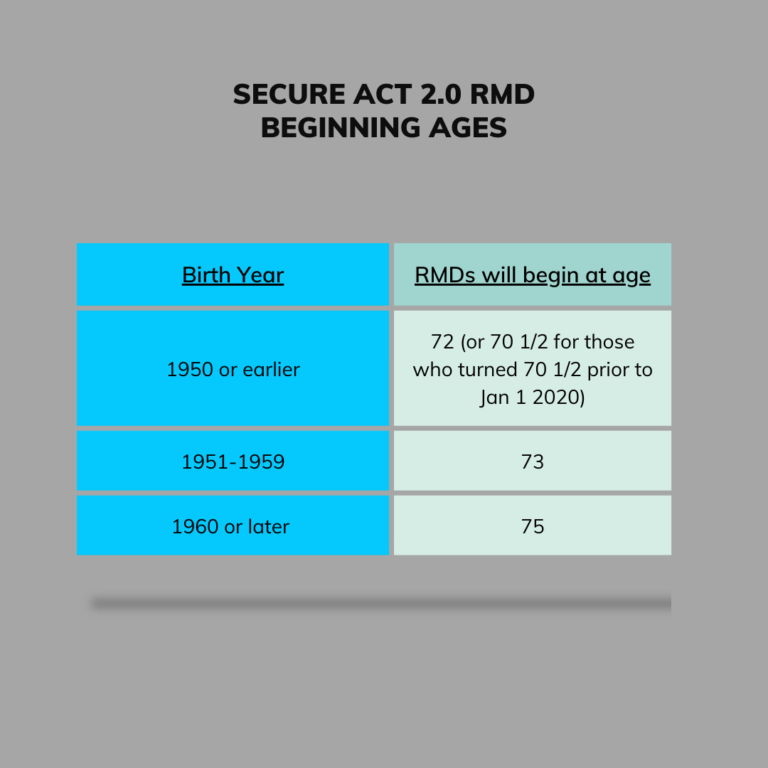

A Roth conversion can eliminate or reduce your required minimum distributions. Required Minimum Distributions (RMDs) are mandatory withdrawals from traditional retirement accounts (IRAs, 401ks, 403bs, TSPs, 457bs, etc.) that the IRS requires once you reach a certain age. The beginning age is currently 73 if you were born before 1960, or 75 if you were born in 1960 or later. RMDs could potentially push your income into higher tax brackets later in retirement when spending actually might go down. Furthermore, if you don’t need all that income, it forces you to realize it anyway to avoid the 25% penalty for a missed RMD.

4. Save Money on Medicare Premiums

Many people don’t realize that when you sign up for Medicare, you might find yourself paying MORE for Medicare Part B and D. Part A is free, and everyone has the same base premium for B and D. However, the more money you make in retirement, the chances of triggering an “IRMAA” surcharge goes up.

IRMAA stands for Income-Related Monthly Adjustment Amount. There are 5 different premium tiers, and each tier increases your IRMAA surcharge. You can also look at it like an excise tax. The more you’ve saved in tax-deferred vehicles (401ks and IRAs), the higher those RMDs might be. More income from RMDs means your Medicare premiums may go up.

5. Reduce the “Surviving Spouse’s Tax Penalty”

The likelihood that a married couple passes away in the same year is very low. Most of the time, women outlive men, or one spouse outlives the other by many years. This is especially relevant if there is a significant age gap between spouses.

Filing jointly is much more tax-advantaged for most people. The surviving spouse will have to switch to filing single, typically the year following the initial spouse’s passing. This could result in pushing the surviving spouse into a much higher tax bracket than when they could file jointly.

Taking this into consideration to ensure you’re not placing your surviving spouse in an unfair or unfavorable tax situation upon your passing is a compelling reason to convert assets from traditional to Roth.

6. Address Changes from the SECURE Act

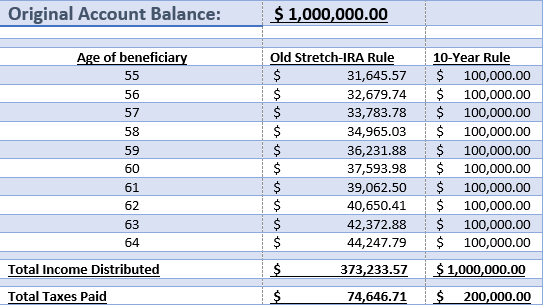

With the SECURE Act going into effect at the end of 2019, we’re seeing the largest acceleration of taxes on retirement assets that we’ve ever experienced. Essentially, the stretch IRA is eliminated for most non-spousal beneficiaries. With the stretch IRA, beneficiaries could “stretch” their IRA withdrawals over THEIR life expectancy. However, the SECURE Act now requires most beneficiaries to liquidate the entire retirement account by the end of the 10th year. This could result in pushing your heirs into an unfavorable tax bracket, especially if they are successful in their own right. We hear all the time that our clients’ children are making more than they ever made! Couple this with large IRAs or 401ks as an inheritance in their peak earning years, and you can see the potential tax trap this brings about. We call it “The Death Tax Trap of 401ks.”

This acceleration of taxes is a big reason to convert from tax-deferred accounts to tax-free accounts. When Roth accounts pass to the next generation, the beneficiaries can enjoy tax-free distributions of the assets instead of tax-deferred distributions.

Understanding the Roth IRA Conversion Process

The concept of a Roth Conversion is essentially to pay the tax now as opposed to deferring those taxes in an IRA or 401k. If you follow the appropriate 5-year rules, everything that grows and compounds in that account, along with the withdrawals, should be tax-free in retirement.

Compare that to a traditional IRA or traditional 401k. These plans give you a tax deduction upfront, but all of that compounding interest and distributions in the back end are taxed as ordinary income in retirement.

Many of my clients over 55 have accumulated the majority of their retirement assets in tax-deferred vehicles, such as 401(k)s and/or IRAs. They may be concerned about the future direction of taxes, particularly given the funding levels of Medicare, Medicaid, and Social Security.

The general concept is: does it make sense to pay taxes now at a potentially lower rate and enjoy tax-free compounding as opposed to tax-deferred compounding going forward?

The Tax Trap of Traditional 401(k)s and IRAs

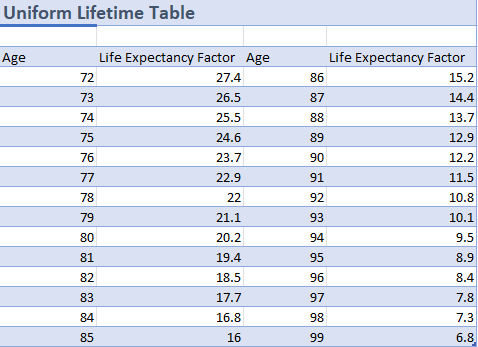

The impact of Required Minimum Distributions are oftentimes one of the biggest tax traps of 401ks and IRAs. Because our clients were diligent savers during their working years, they accumulated substantial assets in 401(k) plans and IRAs. When they turn 73 or 75, they’re forced to take out a certain percentage of those retirement accounts each year.

As your life expectancy shortens, the amount you’re required to take out increases. You start out at a little under 4%, and by the time you get to 90, you’ll be taking out north of 8% of your retirement account, whether you need it or not.

Think about what that can do to your taxable income, Medicare premiums, and ultimately, how those assets are passed on to the next generation. This tax trap is what we’re trying to solve well before clients hit that magic age.

Planning for Longevity in Retirement

More and more people are living longer, often into their 90s. The life expectancy of a 62-year-old female includes a 30% chance of living until 96. When planning with clients over 55 or 60, we may be looking at a retirement of 30 years or more, even longer than their working years.

You must consider this in light of the high inflation we have experienced these past few years. The cost of goods going up over that retirement period on a potentially fixed income is worrisome for many clients. That’s what we try to plan for and mitigate inflation risk coupled with longevity risk.

The Retirement Red Zone

I call the period ten years before you retire and the ten years after you retire the “Retirement Red Zone.” Decisions are magnified, and mistakes are magnified if you make the wrong move.

From an investment perspective, that’s important, especially during volatile times. Certainly, from a tax perspective, which also contributes to the long-term rate of return on your portfolio. This is something I aim to help my clients with as they prepare.

Strategic Planning for Retirement Success

While nobody can predict the future of taxes, you can take the known variables and project out your estimated lifetime tax rates. You will find that throughout retirement, there could be some opportunistic times when your income goes way down. If you’re making strategic moves during that time frame, such as Roth conversions, that planning can help position your retirement assets for better long-term growth and tax efficiency.

Remember, the planning doesn’t stop after retirement, it just changes. Whether you are on the brink of retirement or you’ve been retired for several years, having good guidance at every stage of the process is crucial for achieving financial peace and security in retirement.

Take a deeper dive into this topic by listening to Episode 10 of The Planning for Retirement Podcast. This is for general education purposes only and should not be considered as tax, legal or investment advice. At Imagine Financial Security, we help individuals over 50 with at least a million dollars saved navigate these complex retirement decisions.

If you are looking to maximize your retirement spending, minimize your lifetime tax bill, and worry less about money, you can start with our Retirement Readiness Questionnaire linked on our website at www.imaginefinancialsecurity.com. Click the “Start Now” button to learn more about our process and how we might be able to help you achieve a more confident retirement.

Not quite ready to take the questionnaire, but want helpful tips and resources? Sign up for our monthly newsletter and/or subscribe to our YouTube channel.