Blended Families – You Need a Long-term Care Plan!

As I discussed in a previous article, Long-term Care Planning, I mentioned the fact that 40% of retirement aged clients have long-term care insurance. If you read that article, you understand that I am agnostic as to what the solution is, but we need to have a plan.

These are some questions to get you started:

- Where will care be provided? If care is provided at home, you will likely have family providing the bulk of the care. On top of this, you might hire some professional help to give relief for the family members. If you need specialized care in a nursing home or memory care, the price tag goes up substantially. Check out Genworth’s stats on this below.

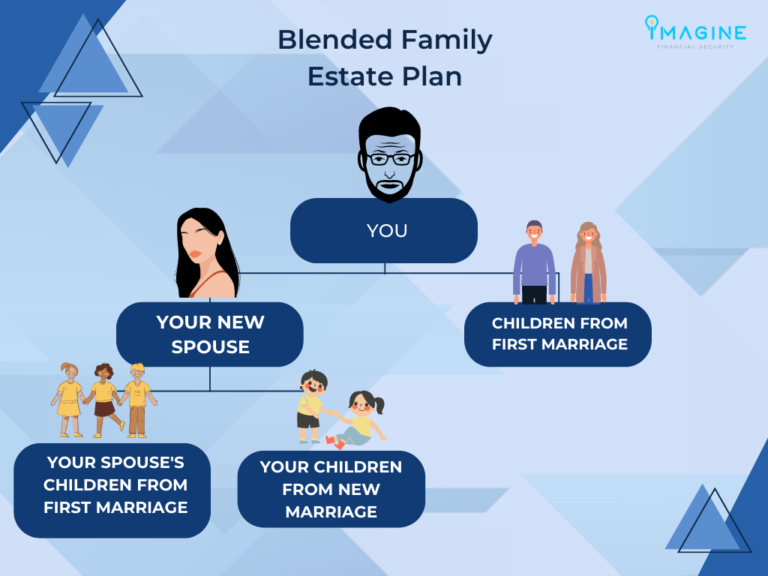

- What assets will be used to pay for care? Different accounts will have different tax consequences. Additionally, certain accounts are better to spend during your lifetime instead of leaving to your children. Make sure you designate which accounts (in order) should be spent down first if there is a long-term care need. Take a look at our article on how to divide assets in a blended family.

- What’s the strategy to mitigate the tax impact of accelerated withdrawals? You might have multiple accounts to draw from, and accelerated withdrawals on certain accounts like 401ks or IRA’s might push you into a higher tax bracket. Additionally, it could result in higher Medicare premiums as a result of “IRMAA” (income related monthly adjustment amount). Therefore, you might work with a fiduciary financial planner who also does tax planning to ensure you are making tax efficient withdrawals.

- Who is the caregiver coordinator? This job can feel like a full time job, even if the individual isn’t the one providing the care. The ongoing hiring, firing, financing, and other issues can result in major headaches for the coordinator. For blended families, what if that coordinator isn’t your biological child? Or, what if your biological child is the coordinator for your new spouse (their step parent)? These are touchy issues and can cause a divide amongst the family. It’s very important to be proactive with all of the children on who is responsible for what. You also might consider hosting a family meeting so all of the children are on the same page.

- Who is going to manage the assets? If you plan to hire professionals to provide the care, some additional asset management will need to be considered. Which investments are being sold when? How does selling those investments impact the long term viability of the portfolio? What’s the tax consequence of selling an investment to pay for care? How does selling an asset impact your legacy goals?