We’ve all heard the sales pitches! “Permanent life insurance solves all of your problems!”

For those of you who have followed me for a period of time know I don’t believe this to be true. But at the same time, there is a large % of the financial advisor (and talking heads) population that blanketly tells people, “Don’t ever buy permanent life insurance.”

To me, this is a breach of fiduciary duty. Just because we all have our biases doesn’t mean we should PUSH those biases on someone’s personal financial situation. As my friend Cody Garrett likes to say, “Keep Finance Personal.”

1. 70% of Americans over 65 will need long-term care during their lives.

2. Fewer than half of you over the age of 65 own insurance to pay for long-term care. Essentially, you are planning to self-insure for long term care.

3. This is the crazy part. 70% of the care being provided is done by unpaid caregivers! Aka. family members…🤔

I wrote about long-term care planning before, but my convictions on this have only increased over the years.

In my previous article, I talked about considerations on whether or not you should purchase insurance.

We also just finished recording a three-part series on The Planning for Retirement Podcast (PFR) about how to fund long-term care costs. Episodes 22 and 23 were about using long-term care insurance and episode 24 was about how to self fund long-term care.

So why do these statistics bother me?

If the majority of retirees will need care, and they are intentionally not buying insurance, that means they plan to self fund for long term care(by default). However, why are family members providing the majority of long term care and not hired help!?

The answer: because there was no real plan to begin with. In reality, it was a decision that was never addressed, or perhaps in their mind they decided to “self fund.” However, that decision was never communicated to their loved ones.

Let me ask you. If you are in the majority that plans to self fund, what conversations have you had with your spouse? Your power(s) of attorney? Your trustee(s)? Do they know how much you’ve set aside if long term care was ever needed? Do they know which accounts they should “tap into” to pay for long-term care?

The chances are “no,” because I’ve never met a client who did this proactively on their own. Ever. And I’ve been doing this for 15 years.

So, this article is for you if you are planning to bypass the insurance route and use your own assets to “self fund long-term care.” I believe this is one of the most important decisions you can make when planning for retirement because it can save how you are remembered.

How much should I set aside to self insure long term care?

It is impossible to pinpoint the exact number YOU will need for care. But let’s pretend your long-term care need will fall within the range of averages.

On average, men need care 2.2 years and women 3.7 years.

The 2021 cost of care study by Genworth found that private room nursing homes cost $108,405/year. Assisted living facilities cost $54,000/year. These are national averages, and the cost of care varies drastically based on where you live.

So let’s use this ballpark figure of $118,800 – $238,491 for men, and $199,800 – $401,098 for women (2.2x the averages for men and 3.7x the averages for women).

The major flaw in using this math is that most people have some sort of guaranteed income flowing into their bank accounts.

Social Security Income

Pensions

Required Minimum Distributions

Of course, not all of that income could be repurposed, especially if you are married. However, perhaps 25%, 50% or 75% of that income could be repurposed for caregivers.

Let’s say you are bringing in $100k/year between Social Security, Pension, and Required Minimum Distributions. Let’s say you are married, and all of a sudden need long term care. For simplicity’s sake, your spouse needs $50k for the household expenses. The other $50k could be repositioned to pay for long-term care. After all, if you need care, you probably are not traveling any longer, or golfing 5 days/week. This unused cash flow can now be dedicated to hiring professional help and protecting your spouse from mental and physical exhaustion.

If we assume the high-end range for men of $238,491, but we assume that $110,000 could come from cash flow (2.2 years x $50k of income), then only $128,491 of your assets need to be earmarked to self fund long term care.

Hopefully, that’s a helpful framework and reassurance that trying to come up with the perfect number is virtually impossible. After all, you may never need care. Or, perhaps you will need care for 5+ years because of Alzheimer’s.

My key point in this article is to address this challenge early (before you turn 60), and communicate your plan to your loved ones.

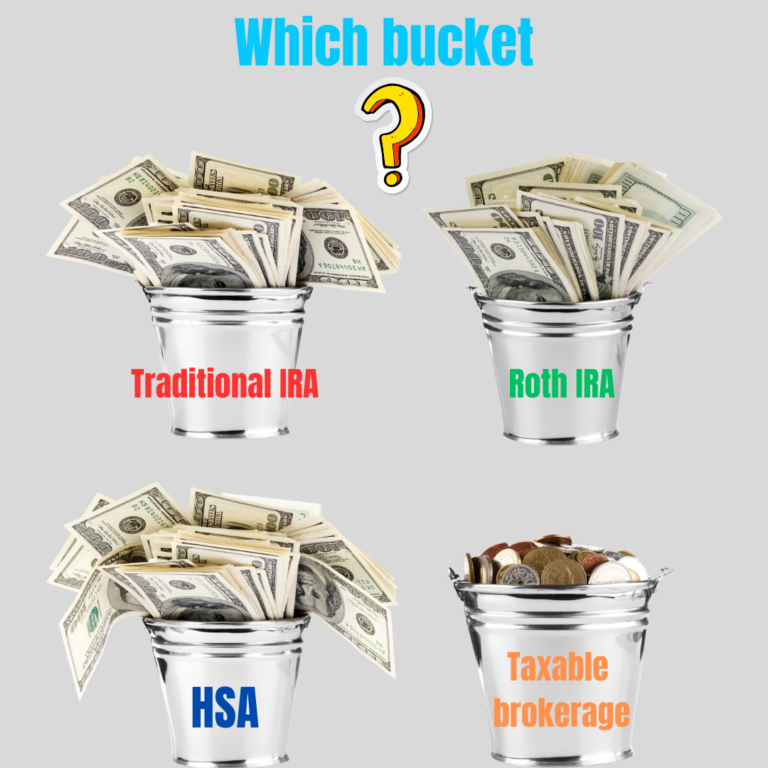

What accounts are the best to self insure long term care?

My personal favorite is the Health Savings Account, or HSA. I wrote in detail about HSA’s in another blog post that you can read here.

Here’s a brief summary:

You can qualify to contribute to an HSA if you have a high-deductible health plan.

The contributions are “pre-tax.”

Earnings and growth are tax-free (you can invest the unused HSA funds like a 401k or other retirement plan).

Distributions can also be tax-free if they are used for “qualified healthcare costs.”

What is a qualified healthcare cost?

Look up IRS publication 502 here, which is updated annually.

One of the categories for qualified healthcare costs is in fact long-term care! This means you can essentially have a triple tax-advantaged account that can be used to self insure long-term care in retirement.

However, you need to build this account up before you retire and go on Medicare. Medicare is not a high-deductible health plan!

But, if you have 5+ years to open and fund an HSA, it can be a great bucket to use in your retirement years, particularly long-term care costs.

The 2023 contribution limits are $7,750 if you are on a family plan and $3,850 if you are on a single plan. There is also a $1k/year catch-up for those over 55.

So, if you’re 55, you could add up to $43,750 in contributions for the next 5 years. If you add growth/compounding interest on top of this, you are looking at 6 figures + by the time you need the funds for care in your 80s. Not bad, right?

Taxable brokerage accounts or "cash"

This bucket is another great option. Mostly because of the flexibility and the tax advantages of taking distributions. Unlike a 401k or IRA, these accounts have capital gains tax treatment. For most taxpayers that would be 15%, which could be lower than your ordinary income tax rate (it could also be as low as 0% and as high as 20%+).

If you are earmarking some of these dollars for care, I would highly recommend two things:

Separate the dollars you intend to spend for care and give this new account a name (“long-term care account”)

Invest the account assuming a time horizon for your 80s instead of your 60s. In essence, you can make this account more aggressive in order to keep pace with the inflation rate for long term care expenses.

What’s nice about this bucket is that it’s not a “use it or lose it.” Just because you segregated some assets to pay for care, doesn’t mean those dollars have to be used for care. When these dollars pass on to the next generation, they should receive a step up in cost basis for your beneficiaries. If the dollars are in fact needed for care, you will only pay taxes on the realized gains in the portfolio.

🤔 Remember when we talked about tax loss harvesting in episode 19? Well, this strategy could also apply to help reduce the tax impact if this account is used to self-insure long-term care.

Of course, cash is cash. No taxes are due when you withdraw money from a savings account or a CD. Now, I wouldn’t suggest using a CD or cash to self-insure care, simply because it’s very likely that account won’t keep pace with inflation. However, if there is some excess cash in the bank when you need care, this could be a good first line of defense before the more tax-advantaged accounts are tapped into.

Traditional 401ks and IRAs

This bucket is often the largest account on the balance sheet when you are 55+. However, many advisors and financial talking heads recommend against tapping these accounts to self insure long term care because of the tax burden.

Well of course, it may not be ideal as a first line of defense to pay for care, but if it’s your only option, “it is what it is.”

But here’s the thing. If you are needing long term care, you’re most likely over the age of 80. This means you are already taking Required Minimum Distributions or RMDs. If you have a $1mm IRA, your RMD would be $62,500 at age 85. Let’s say you also have Social Security paying you $24,000/year. That’s a total income of $86,500 that is coming into the household to pay the bills. This was my point earlier in that you likely have income coming in that can be repurposed from discretionary expenses to hiring some professional help for care.

This means that you may not need to increase portfolio withdrawals by a huge number if RMDs are already coming out automatically.

But yes, you’ll have taxes due on these accounts based on your ordinary income rates. And yes, if you increase withdrawals from this bucket, this could put you in a position where your tax brackets go up, or your Social Security income is taxed at a higher rate, or perhaps will have Medicare surcharges.

On the flip side, this could also trigger the ability to itemize your deductions due to increased healthcare costs. In fact, any healthcare costs (including long term care) that exceed 7.5% of your adjusted gross income could be counted as a tax deduction (as of 2023).

The net effect essentially could be quite negligible as those additional portfolio withdrawals could be offset with tax deductions, where applicable.

Life Insurance and Annuities

Maybe you bought a life insurance policy back in the day that you held onto. Or you purchased an annuity to provide a guaranteed return or guaranteed income. However, you may find that your goals and circumstances change throughout retirement. Perhaps your kids are making a heck of a lot more money than you ever did, so they don’t have a big need for an inheritance. Or, that annuity you purchased wasn’t really what you thought it was. You could look at these accounts as potential vehicles to self-insure for long term care.

Life Insurance could have two components – a living benefit (cash value) and a death benefit. In this case, you could use either or as the funding mechanism for long term care.

Let’s say you have $150k in cash value and a $500k death benefit. Instead of tapping into your retirement accounts or brokerage accounts, you could look at borrowing or surrendering your life insurance cash value to pay for care. Or, you could look at the death benefit as a way to “replenish” assets that were used to pay for care.

Annuities could be tapped into by turning the account into a life income, an income for a set period of time, or as a lump sum. All of those options could be considered when it comes to raising cash for this type of emergency.

Roth Accounts

This is the second most tax-efficient retirement vehicle behind the HSA. It’s not only a great retirement income tool, but it’s also a great tool to use for financial legacy given the tax-free nature from an estate planning perspective. However, this account could be used to self insure long term care without triggering tax consequences.

Let’s say you need another $30k for the year to pay for care. But an additional $30k withdrawal from your traditional 401k would bump you into the next tax bracket. Instead, you could look to tap into the Roth accounts in order to keep your tax bracket level.

Home equity

The largest asset for most people in the US is their home equity. However, people rarely think of this as a way to self insure long term care. In fact, this is why many caregivers are family members! They want their loved ones to stay at home instead of moving into a nursing home. But perhaps there isn’t a huge nest egg to pay for care. If you have home equity, you could tap into that asset via a reverse mortgage, a cash-out refinance, or a HELOC. There are pros and cons of each of these, but the reverse mortgage (or HECM) is a great tool if you are over the age of 62 and need access to your equity.

The payments come out tax-free, the loan doesn’t need to be repaid (unless the occupant moves, sells, or dies), and there are protections if the value of the home is underwater.

Inform your key decision makers

Now that you have a decent understanding of how much to set aside and which accounts might be viable for you, it’s time to have a family meeting.

If you’re married, have a conversation with your spouse.

If you have children, bring them into the discussion, especially those that will have a key decision-making role (powers of attorney, trustee etc).

You know your family dynamic best. The point you need to get across is that you do have a plan to self insure long term care despite not owning long term care insurance. Your loved ones need to know how much they could tap into (especially the spouse) in the event you need care. This is very important, give your spouse permission to spend! Being a caregiver, especially a senior woman, will very likely result in burnout, stress, physical deterioration, mental exhaustion, and resentment. If you simply leave it to your spouse to “figure out,” they will always resort to doing it themselves in fear of overspending on care.

❌ Don’t do this to them!

I hope you found this helpful! Make sure to subscribe to our newsletter below so you don’t miss any of our retirement planning content! Until next time, thanks for reading!

This is part 2 of 3 in our series, “How to pay for Long-term care costs in retirement.”

Rodney Mogen and Peter Ciravalo from BC Brokerage are my guests again today and they bring a ton of knowledge on this topic! There is a reason Hybrid Long-term Care policies make up the majority of insurance products sold today. However, because there are so many different types of products and how they fit into a client’s situation, oftentimes retirees and pre-retirees can feel overwhelmed with where to start.

I hope you enjoy this episode and make sure to hit “FOLLOW” so you don’t miss out on part 3, “How to self-fund extended care costs in retirement.”

Despite two major US banks failing, coupled with central banks’ attempt to fight persistent inflation, the US and International markets experienced some positive momentum!

The Banking System

One of our recent articles was about the collapse of Silicon Valley Bank (SVB), the 2nd largest US bank failure in history. This sent a ripple effect into the banking system, particularly a flight of deposits from smaller regional banks to big banks.

JP Morgan posted a 52% jump in its first-quarter profits.

Wells Fargo topped analysts’ projections by 10 cents a share in Q1.

Citigroup also beat analysts’ estimates on revenue.

In short, customers were worried that their bank might also fail following SVB and Signature’s collapse. As I discussed in our previous post, which you can read here, SVB and Signature were heavily concentrated on client bases that had unique challenges in this economy (tech industry and crypto).

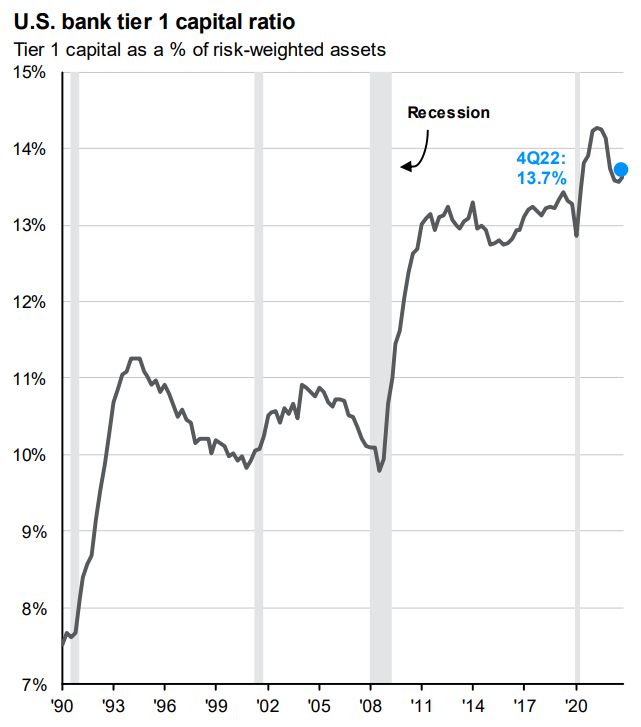

However, bank capitalization looks very healthy and has been on the uptrend since 2008 following the Global Financial Crisis. This is one positive impact of tighter regulation on big banks following The Great Recession.

Source: JP Morgan Asset Management

The real fallout

Despite big banks experiencing an inflow of deposits from smaller banks, they are still facing tighter lending standards and rapidly increasing interest rates. They now have to pay us all higher yields in return for their money market or CD accounts. Smaller and more regional banks, however, will face a reductionin deposits AND increased lending standards. Regulators and board members are going to be watching like a hawk to ensure more banks don’t have the same risks that SVB and Signature Banks did.

As banks tighten their lending standards, individuals and businesses are going to struggle to get loans. Individuals who could previously afford that new or used vehicle might not qualify any longer. Or, people shopping for their first home can’t afford the mortgages given the rapid uptick in rates.

Businesses that rely on these smaller and regional banks for loans to keep their lights on or survive this challenging market will find it harder to get capital.

All of these ripple effects will contribute to a slowing economy.

But after all, this was the Fed’s goal ever since they announced their rate hike and quantitative tightening strategy back in 2021. Their main objective was to fight inflation, and they needed to slow the economy in the short run to win the battle in the long run.

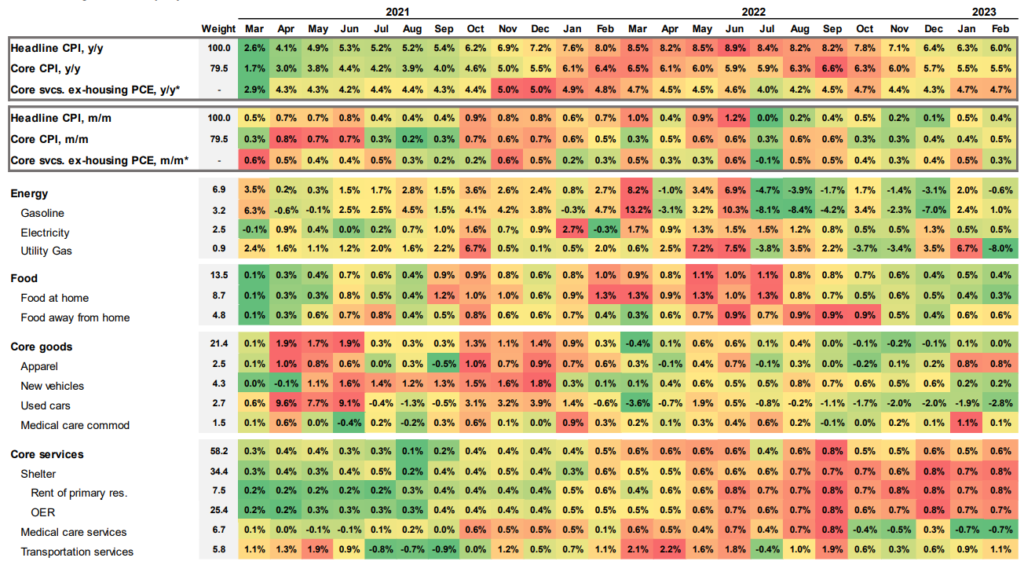

Speaking of inflation...

After setting 40-year highs in 2022, inflation is finally cooling a bit. The peak was 8.9% in June, but we’ve seen a gradual decline ever since. The March numbers were just released and showed a 5% year-over-year CPI figure. The Fed’s target overall is 2%, so we are still a ways from that number. Despite the trend going in the “right” direction, I don’t believe the Fed will get all the way to their 2% goal unless unemployment falls exponentially over the coming months. The cooling inflation story is the primary reason the market has rallied since the start of 2023. Inflation under check means the Feds might actually STOP raising interest rates very soon. The market is pricing in one more 0.25% rate hike and then the expectation is rates will level off and eventually fall in 2024.

The real question is, has the Fed done so much damage with its policy that they send the economy into a recession? If this happens, they could even pivot to rate cuts as early as the end of 2023 or the beginning of 2024. My hope is that they take a pause and let the economy settle itself out.

Source: JP Morgan Asset Management

Unemployment and Wages

The unemployment story has been a big part of why inflation has been so sticky.

We entered 2020 with a 3.5% unemployment rate, which was a 50-year low. After topping over 10% unemployment (briefly) in 2020, the US now has a 3.6% rate. Additionally, wage growth is at 5.3%, which is above the historical average of 4%. So, if people are “working” and wages are still growing, it’s no wonder inflation has been so tough to fight. People did not stop spending money in 2022 because of prices going up. Sure, consumer discretionary categories took a hit, but the core goods and services were still being purchased at elevated prices. This is a big reason I don’t believe prices are going to come down as much as the Feds want them to. Why would corporations cut prices when their consumers have the wages to buy them?

One of the chips likely to fall is the unemployment story in big tech firms. Since 2018, Amazon and Meta (Facebook’s parent) have almost doubled their workforce. During that same period, Microsoft increased its workforce by 53%, and Alphabet by 60%! Meanwhile, Apple only grew its workforce at a moderate 20% rate.

Remember the Paycheck Protection Program in 2020? This was a federal loan to corporations to keep their employees on payroll during COVID. All they had to do was use at least 60% of those loans to cover payroll and the “loan” was forgiven. The word on the street is that big tech used their loans to go on massive hiring sprees. Not because they NEEDED that many more workers, but to reduce the talent pool for their competitors and have their PPP loans forgiven! Now that the economy is slowing, we’re seeing big tech begin layoffs. Coincidently, Apple hasn’t laid anyone off just yet.

‘Penned’ tech specialists are earning six-figure salaries to ‘do nothing’ and string out 10-minute tasks. Some are even using the time to scuba dive

Some of the highest unemployment numbers by industry are:

Farming – 7.4%

Mining, quarrying, oil and gas extraction – 6.5%

Construction – 5.6%

Leisure and Hospitality – 5%

Transportation and utilities – 4.6%

Meanwhile, big tech unemployment is only at 2.6%, up from 1.5% to start the year. All of the remote workers that migrated out of the big cities during the pandemic are now experiencing some layoff concerns, and it will be very interesting to follow that narrative as big tech continues to cut their unnecessarily large workforces.

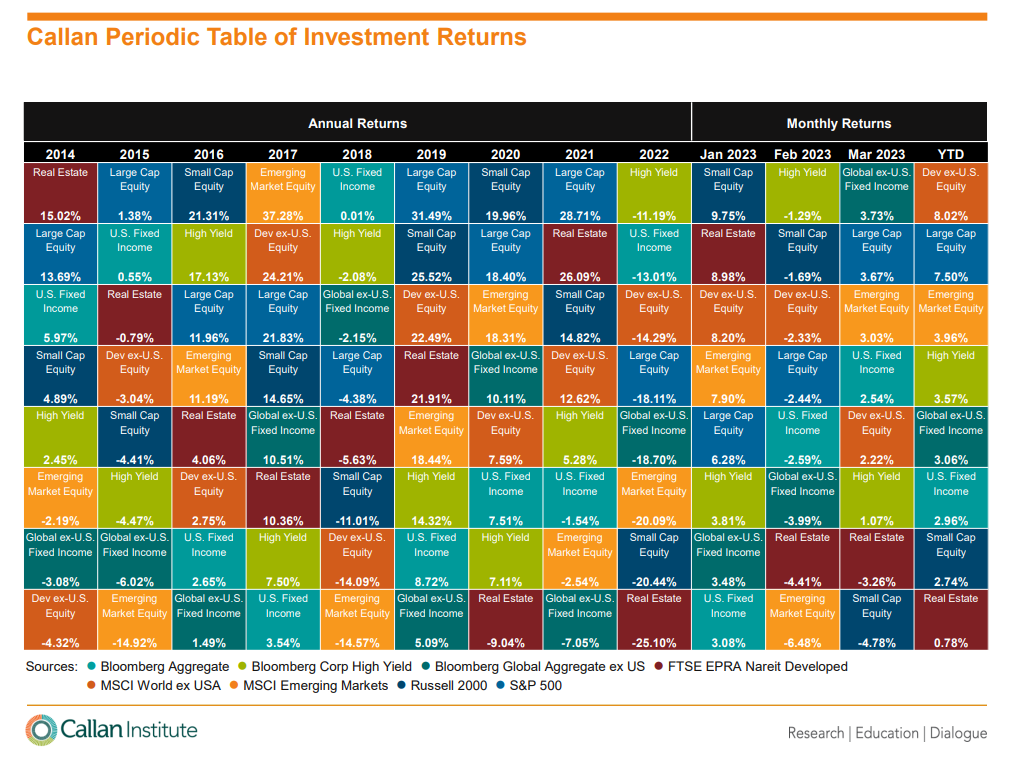

Returns by asset class, YTD

As you can see year to date, all of the major asset classes are positive. International, developed economies are in the top spot, with US Large Cap a close second. What’s very encouraging is that the fixed-income markets are now showing positive returns after a rough 2022.

During the re-balancing process for our clients at the beginning of 2023, the only asset classes we added exposure to were Large Cap Growth companies (big tech) and international equities. This isn’t to pump our chest to say “I told you so.” However, part of our process is to sell the winners and buy the losers. Big tech was the worst-performing asset class in 2022, and stock performance is a leading indicator. What I mean is, the layoffs and bad news for big tech this year were already priced into the market in 2022 (at least we hope so). We talked a lot about interest rate increases during 2021 and 2022 and how it would impact tech companies. After the brutal selloff in 2022, valuations looked much more attractive going into 2023…hence, buying the loser. So far year to date it’s paid off well, but that’s not to say there isn’t more volatility ahead for big tech with the challenging interest rate environment they face.

The same can be said about international equities as they had a rough go in 2022 but are very well positioned from a valuation perspective for the decade ahead. International stocks tend to do well during periods of high inflation, like in the 70s and 80s. However, geopolitical concerns with Russia/Ukraine and China still make international stocks much more volatile.

Final thoughts

Attempting to time the market is very dangerous. If you look back at the past year, consumer sentiment has been at record lows. People have not been feeling good about the economy. This feeling oftentimes leads to investors flighting to safety. How many articles have you seen about I-Bonds or CD Rates over the last 12-18 months? Well, stock market returns typically accelerate very quickly after a recovery. In fact, more than 50% of the best daily S&P 500 returns occur during a bear market. So if you bailed out during 2022, you did not get the benefit of a strong Q1 in 2023!

While we are going to be experiencing a tighter economy for the foreseeable future with higher rates, there is now hope with the inflation story beginning to unfold. Let’s hope the market is correct in that the Fed will only increase rates one last time at 0.25% and be finished. The unemployment and wage growth figures will be key to watch over the coming months as that will dictate how quickly inflation comes down in late 2023.

If you are curious about how the market has impacted your financial goals, we’d love to hear from you! You can either send me an email at kevin@imaginefinancialsecurity.com or book a Zoom call with us.

In my nearly 14 years in this business, I’ve seen financial advice given by many different professionals. Insurance agents, stock brokers, bank representatives, real estate professionals, next door neighbors and the like. I’ve seen some great advice given, but also some terrible advice. This often times leads to the general public to think “are financial advisors worth it?” This is especially the case now given the lines are blurred between different segments of the “financial services” industry. Vanguard did a study called “Advisor’s Alpha” which I have found is the most helpful and accurate summary of value-added services a comprehensive financial advisor provides. I’ve referenced it to clients and other professionals since 2014 when it was originally published. To summarize it briefly, they outline seven areas of advice that add value to the client’s portfolio by way of net returns annually. They have assigned a percentage to each of the categories which amounts to approximately 3%/year in net returns! In this article, I will highlight some of the key components of their research, as well as put my own spin on it based on my thousands of hours working with clients directly.

What is comprehensive advice?

First things first, not all advisors are comprehensive (and that’s okay). However, this article is specifically for firm’s like mine that are focused on comprehensive advice and planning, and I would argue the 3%/year figure is on the low end. I will get into this more shortly.

Here is a breakdown of Vanguard value-added best practices that I mentioned previously:

The first thing that should jump out to you is that suitable asset allocation represents around 0%/year! This is given the belief that markets are fairly efficient in most areas, and it’s very difficult for an active fund manager to consistently beat their benchmarks. This is contrary to the belief of the general public in that a financial advisors “alpha” is generated through security selection and asset allocation! What’s also interesting is that the largest value add is “behavioral coaching!” I will get into more about what this means, but I would 100% agree with this. Sometimes, we are our own worst enemy, and this is definitely true when it comes to managing our own investments. It’s natural to have the fear of missing out, or to buy into the fear mongering the media portrays. So if you take nothing else away, the simple notion of having a disciplined process to follow as you approach and ultimately achieve financial independence will add 150% more value than trying to pick securities or funds that may or may not outpace their benchmarks!

Before I dive into my interpretation of their study, I want to note that I will be using five major categories instead of seven. Some of the above mentioned can be consolidated, and there are also some value added practices I, and many other comprehensive planners, incorporate that are not listed in their research.

What are the five value-added practices? I use the acronym “T-I-R-E-S”

Tax planning

Income Distribution Planning

Risk Management

Expense Management

Second set of eyes

Tax planning

There are four major components of tax planning a comprehensive financial advisor should provide. The first component is what we call “asset location.” The saying that comes to mind is “it’s not what you earn, it’s what you keep.” Well, taxes are a perfect example of not keeping all that you earn. However, some account types have preferential tax treatment, and therefore should be maximized through sound advice. Certain investments are better suited for these types of tax preferred accounts and other investments tend to have minimal tax impact, and therefore could be better suited OUTSIDE of those tax preferred accounts. A prime example is owning tax free municipal bonds inside of a taxable brokerage or trust account, and taxable bonds inside of your IRA or Roth IRA’s. Another example could be leveraging predominantly index ETF’s within a brokerage account to minimize turnover and capital gains, but owning a sleeve of actively managed investments in sectors like emerging markets, or small cap equities inside of your retirement accounts. According to the Vanguard study, this type of strategy can add up to 75 basis points (0.75%/year) in returns if done properly, which I would concur.

The second component is income distribution. This is often thought of much too late, usually within a few years of retirement. However, this should be well thought out years or decades in advance before actually drawing from your assets. One example I see often is when a prospective client who is on the brink of retiring wants a comprehensive financial plan. Often times they have saved a significant sum of money, but the majority of the assets are held inside of tax deferred vehicles like a 401k or IRA, and little to no assets in a tax free bucket (Roth). This type of scenario limits tax diversification in retirement. On the contrary, someone who has been advised on filling multiple buckets with different tax treatments at withdrawal will have many combinations of withdrawal strategies that can be deployed depending on the future tax code at the time. I have incorporated the rest of the income distribution value-added practice in the next section, but this practice as a whole is estimated to add up to 110 basis points (1.1%/year) in additional returns!

Legacy planning is the third component of tax planning that a comprehensive financial advisor should help with. This isn’t discussed in the Vanguard study, but it’s safe to say a comprehensive plan has to involve plans for your inevitable demise! You might have goals to leave assets to your heirs, especially if you are fortunate enough to have accumulated more than you will ever spend in your lifetime. With the SECURE Act, qualified retirement plans are now subject to the “10-year rule,” and therefore accelerating tax liabilities on your beneficiaries. However, if you incorporate other assets for legacy that can mitigate the tax impact on the next generation, this can save your beneficiaries hundreds of thousands, or even millions of dollars simply by leveraging the tax code properly.

Finally, navigating tax brackets appropriately can be another way a comprehensive advisor adds value. If a client is on the brink of a higher tax bracket, or perhaps they are in a period of enjoying a much lower tax bracket than normal, planning opportunities should arise. If you are in an unusually higher tax bracket than normal, you might benefit from certain savings or tax strategies that reduce their adjusted gross income (think HSA’s, pre-tax retirement account contributions, or charitable giving). If you find yourself in a lower tax bracket than normal, you might accelerate income via Roth conversions or spending down tax deferred assets to lessen the tax burden on those withdrawals. Additionally , considerations on the impact on Medicare premiums in retirement should also be taken into account when helping with tax planning.

As you can see, even though I am not a CPA and I’m not in the business of giving tax advice, helping you be strategic with your tax strategies is part of the comprehensive planning approach. All in, you should expect to increase your returns up to 1%/year (or more depending on complexity) by navigating the tax code effectively.

Income Distribution Strategy

In my personal practice, this ends up being a significant value add given the work I do with post-retirees. A systematic withdrawal strategy in retirement will involve a monthly distribution 12 times throughout the year. This reduces the risk of needing a sizeable distribution at the wrong time (similar to the concept of dollar cost averaging). For a 30 year retirement, this means 360 withdrawals! Most retirees have at least two different retirement accounts, so multiply 360 by 2 for 720 different income decisions to navigate. In my experience, the selling decisions are often what set investors back, especially if they are retired and don’t have the time to make it back. By putting a process in place to strategically withdrawal income from the proper investments at the right time, and maximize the tax efficiency of those withdrawals, this can add up to 1.1%/year in returns alone, according to Vanguard’s study! I’ve also had clients tell me they value their time more and more the older they get. Instead of spending their retirement managing income withdrawals each month, they would much rather travel, play golf, go fishing, spend time with their grandchildren etc. So yes, I would agree with the Vanguard study that 1.1%/year is appropriate for this category, but I would also argue the peace of mind of not needing to place trades while you are on an African Safari with your spouse is priceless! Yes, I did have a client who admitted to this, and no, his wife was not happy! That’s why they hired me!

Risk Management

The major risks you will see during your lifetime from a financial planning perspective are:

Bear market

Behavioral

Longevity

Inflation

Long-term care

Premature death

Incapacity or aging process

Vanguard’s study focuses mainly on the behavioral risk (value add up to 1.5%/year) and re-balancing (.26%/year). As I mentioned earlier, it’s fascinating they rank behavioral risk as the largest value add out of any category! What is behavioral risk? Let me tell you a quick story. A client of mine was getting ready to retire at the beginning of 2020, right as the pandemic reared it’s ugly head. He had 30+ years working in higher ed and climbed the ladder to ultimately become president of his college for the last 15 years. He is a brilliant man, and a savvy business person. When the pandemic hit us, he was terrified. Not only did he see his portfolio drop from $2.5mm to $2.25mm in four weeks, but he was worried this could lead to the next depression which his parents lived through. We had at least a dozen conversations during those weeks about how he was losing sleep every night, which of course was miserable for he and his wife. Finally, in our last discussion he informed me he wanted to sell out of his retirement investments and move to cash. I plead my case in that we had a well thought out diversified strategy, and looking at the math, we had enough resources in fixed income investments to pay his bills for the next ten years! However, I told him it was his money and I was ready to place the trades if that is what he wanted. He told me he would think on it for the next 24 hours. The next day, he called me and said I was right, we had a plan, and he wanted to proceed with sticking to the plan. Well, by the end of 2020 his account not only fully recovered, but it grew to $2.75mm! I am not pumping my chest on performance, but by being the behavioral coach he needed at that time earned him $500k of growth in his portfolio (a whopping 22%).

I can literally share a hundred of these stories not just from the pandemic, but stories from 2008/2009, the dot com bubble etc. The point is, having an advisor you trust that can help you navigate through the ups and downs of the market and tell you what you NEED to hear, not what you WANT to hear is invaluable. Furthermore, it can free up your time to focus on what matters in your life and have the professionals worry about the market for you!

So all in all, I would agree on the 1.5%/year value add for behavioral coaching and .26%/year to help re-balance the portfolio properly. However, Vanguard’s study doesn’t even take into consideration proper insurance planning and estate planning advice a comprehensive advisor gives to their clients which are also value-adds in and of themselves. In that sense, I would argue this category can add up to 2%/year in additional returns to a client.

Expense Management

This is oftentimes overlooked when working with a financial advisor. Much of the public believes working with an advisor will be more expensive! However, many of them are used to being sold high commission investment products or services that are overpriced. However, through due diligence and leveraging the proper research, Vanguard estimates clients should save on average 0.26%-0.34%/year on expenses. From my personal experience, this might even be on the low end. However, for arguments sake and given it’s their research, let’s say we agree with the value-added range set forth.

Second set of eyes

Vanguard doesn’t reference this in their study, but that objective point of view is sometimes necessary to drive positive change. I don’t have any specific data on how to quantify this, but I hear time and time again from clients that they so much appreciate having me as an accountability partner. Think about trying to get in tip top shape without a coach or personal trainer! You might do okay, but you certainly wouldn’t push yourself as hard as you could have if you had a coach or trainer. On the contrary, I often hear from new prospective clients how information overload and the fear of making a mistake has caused a whole lot of inaction, which can significantly hurt returns and performance. Think about a surgeon attempting to perform surgery on their own body! They simply wouldn’t. Not that I am comparing my occupation to a surgeon, but someone working to achieve financial independence would benefit substantially from a trusted third party to help navigate all of the different financial decisions they will encounter in their lifetime. This also could be true for married couples who might have differing views on finances. After all, financial reasons are the #1 cause for divorce in America. If I can help a married couple get on the same page with their financial vision, that is a win for them, no questions asked! Without specific data, I would have to say my gut feel is that objectivity should add an additional 0.5%/year in returns over the duration of a relationship, as well as more self confidence and peace of mind that you are on the right path.

If we tally up our TIRES acronym:

Tax planning = 1%/year

Income Distribution Planning – 1.1%/year

Risk Management – 2%/year

Expense Management – 0.26% – 0.34%/year

Second set of eyes – 0.5%/year

This gives us a total value add range of 4.86% – 4.94%/year in additional returns. My firm’s average fee is roughly 0.85%/year. This is why I get so excited to help new and existing clients. The value you receive, is far greater than the cost to pay me, creating a win-win situation. Now, not EVERY client will experience in additional 4-5% in additional value. Some might receive 2%/year, some might receive 10%/year! However, all of you who have yet to work with a comprehensive planner, or for those of you working with an advisor who may not be doing a comprehensive job, it might be time to reevaluate and see what holes you need to fill. If you are interested in learning how to work with me directly, you can schedule a mutual fit meeting with the button below. Or, you can visit my “Process” and “Fees” pages on my website.

70% of those 65 and older will need long-term care services. The question is, how will you pay for it? We will address buying insurance vs “self-insuring” in our article.

Have you stress tested your retirement plans? If you are within 10 years of retirement, you must have a plan for the 6 “what-if” scenarios that could derail your financial goals.

The year was 2007, and my parents were all set to retire in just 12 short months. My Dad worked in IT and is a first generation American. My Mom was a preschool teacher and had no retirement benefits. She knew little about what was going on with their financial plans aside from listening to my Dad complain every time the market was down. As we now know, 2007 was the beginning of the Great Recession, which is the worst recession we’ve seen in our lifetime. Stock markets were down close to 50% and unemployment reached 10%. Like many other hard working Americans, the Great Recession of 2008 ended up pushing my parents’ retirement back 11 years. I made it my mission to help every day families prepare for the what-if scenarios when planning for retirement, including:

What if we go through a recession like 2008?

What if one, or both of us live longer than expected?

What if there are changes to Social Security?

What if market returns are lower than we anticipate?

What if there is higher than expected inflation?

What if there is a long-term care event during retirement?

These are the 6 most common concerns that keep my clients up at night. My value proposition is to stress test each one of them and ensure their plans are bulletproof to and through retirement. I look forward to meeting you live at our webinar.

Planning for expected events in Retirement is easy. Planning for the unexpected is wise. These are the top four stress tests to put your Retirement Plans through to see if you are as bullet proof as you need to be.

They say it’s not what you earn, it’s what you keep. I agree with this wholeheartedly as it relates to not spending more than you make (obviously). However, in my line of work, being sensitive to the TAX efficiency of a retirement plan is critical. If I can save my clients $10,000 or even $20,000/year in taxes during retirement, that’s huge!

In a world where it seems like companies are moving away from customer service and towards automation, I wanted to have a practice where the focus was on white-glove service and treating every client like family instead of a number.